Investing money is necessary to survive the increasing cost of living.

1.1 Why should one Invest?

Before we address the above question, let us understand what would happen if one chooses not to invest. Let us assume you earn Rs.50,000/- per month, and you spend Rs.30,000/-towards your cost of living, which includes housing, food, transport, shopping, medical, etc. The balance of Rs.20,000/- is your monthly surplus. For the sake of simplicity, let us ignore the effect of personal income tax in this discussion.

To drive the point across, let us make a few simple assumptions.

The employer is kind enough to give you a 10% salary hike every year.

The cost of living is likely to go up by 8% year on year.

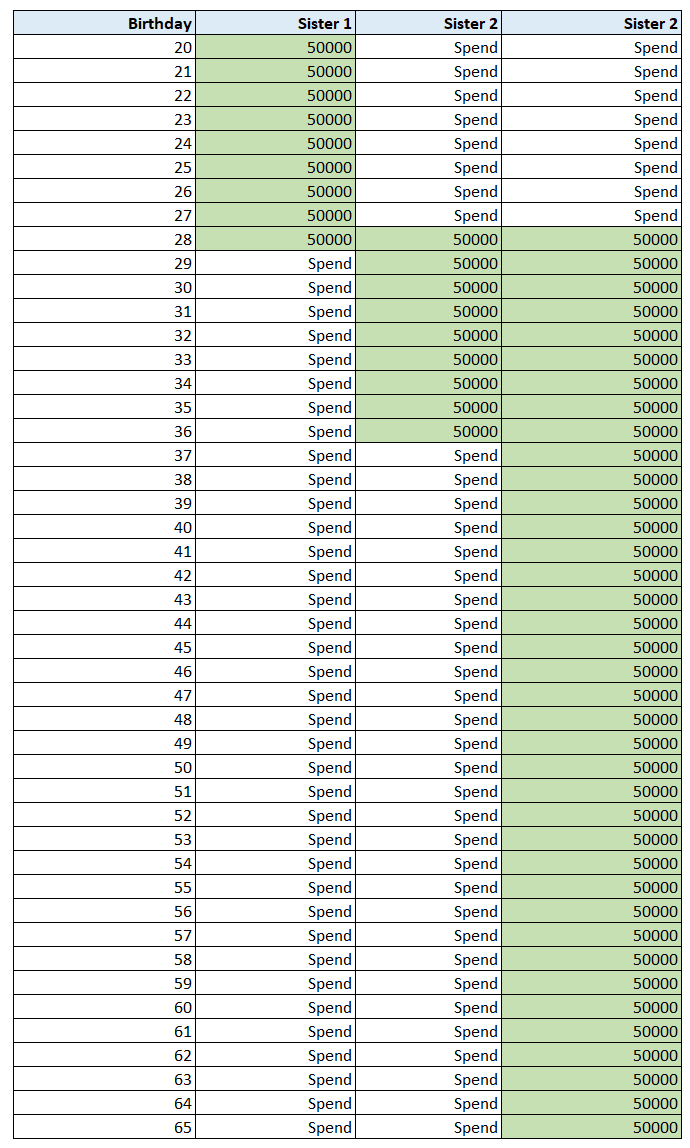

You are 30 years old and plan to retire at 50. This leaves you with 20 more years to earn

You don’t intend to work after you retire.

Your expenses are fixed and don’t foresee any other expense.

The balance cash of Rs.20,000/- per month is retained in the form of hard cash.

Going by these assumptions, here is how the cash balance will look like in 20 years.

Years

Yearly Income

Yearly Expense

Cash Retained

1

600,000

360,000

240,000

2

6,60,000

3,88,800

2,71,200

3

7,26,000

4,19,904

3,06,096

4

7,98,600

4,53,496

3,45,104

5

8,78,460

4,89,776

3,88,684

6

9,66,306

5,28,958

4,37,348

7

10,62,937

5,71,275

4,91,662

8

11,69,230

6,16,977

5,52,254

9

12,86,153

6,66,335

6,19,818

10

14,14,769

7,19,642

6,95,127

11

15,56,245

7,77,213

7,79,032

12

17,11,870

8,39,390

8,72,480

13

18,83,057

9,06,541

9,76,516

14

20,71,363

9,79,065

10,92,298

15

22,78,499

10,57,390

12,21,109

16

25,06,349

11,41,981

13,64,368

17

27,56,984

12,33,339

15,23,644

18

30,32,682

13,32,006

17,00,676

19

33,35,950

14,38,567

18,97,383

20

36,69,545

15,53,652

21,15,893

Total Income

17,890,693

If one were to analyze these numbers, you would soon realize this is a scary situation to be in. Few things are quite startling from the above calculations:

After 20 years of hard work you have accumulated Rs.1.7Crs.

Since your expenses are fixed, your lifestyle has not changed over the years, you probably even suppressed your lifelong aspirations – better home, a better car, vacations, etc.

After you retire, assuming the expenses will continue to grow at 8%, Rs.1.7Crs is good enough to sail you through roughly about 8 years of post-retirement life. 8th year onwards you will be in a very tight spot with literally no savings left to back you up.

What would you do after you run out of all the money in 8 years? How do you fund your life? Is there a way to ensure that you collect a larger sum at the end of 20 years?

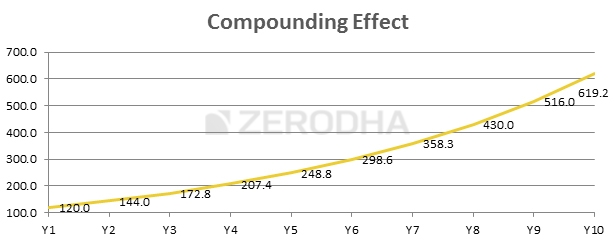

Let’s consider another scenario where instead of keeping the cash idle, you choose to invest the cash in an investment option that grows at let’s say 12% per annum. For example – in the first year you retained Rs.240,000/- which when invested at 12% per annum for 20 years yields Rs.2,067,063/- at the end of 20th year.

Years

Yearly Income

Yearly Expense

Cash Retained

Retained Cash Invested @12%

1

600,000

360,000

240,000

20,67,063

2

6,60,000

3,88,800

2,71,200

20,85,519

3

7,26,000

4,19,904

3,06,096

21,01,668

4

7,98,600

4,53,496

3,45,104

21,15,621

5

8,78,460

4,89,776

3,88,684

21,27,487

6

9,66,306

5,28,958

4,37,348

21,37,368

7

10,62,937

5,71,275

4,91,662

21,45,363

8

11,69,230

6,16,977

5,52,254

21,51,566

9

12,86,153

6,66,335

6,19,818

21,56,069

10

14,14,769

7,19,642

6,95,127

21,58,959

11

15,56,245

7,77,213

7,79,032

21,60,318

12

17,11,870

8,39,390

8,72,480

21,60,228

13

18,83,057

9,06,541

9,76,516

21,58,765

14

20,71,363

9,79,065

10,92,298

21,56,003

15

22,78,499

10,57,390

12,21,109

21,52,012

16

25,06,349

11,41,981

13,64,368

21,46,859

17

27,56,984

12,33,339

15,23,644

21,40,611

18

30,32,682

13,32,006

17,00,676

21,33,328

19

33,35,950

14,38,567

18,97,383

21,25,069

20

36,69,545

15,53,652

21,15,893

21,15,893

Total cash after 20 years

4,26,95,771

With the decision to invest the surplus cash, your cash balance has increased significantly. The cash balance has grown to Rs.4.26Crs from Rs.1.7Crs. This is a staggering 2.4x times the regular amount. This translates to you being in a much better situation to deal with your post retirement life.

Now, going back to the initial question of why invest? There are a few compelling reasons for one to invest.

Fight Inflation – By investing one can deal better with the inevitable – growing cost of living – generally referred to as Inflation

Create Wealth – By investing, one can aim to have a better corpus by the end of the defined time period. In the above example, the time period was up to retirement, but it can be anything – children’s education, marriage, house purchase, retirement holidays, etc

Having figured out the reasons to invest, the next obvious question would be – Where would one invest, and what are the returns one could expect by investing.

When it comes to investing, one has to choose an asset class that suits the individual’s risk and return temperament.

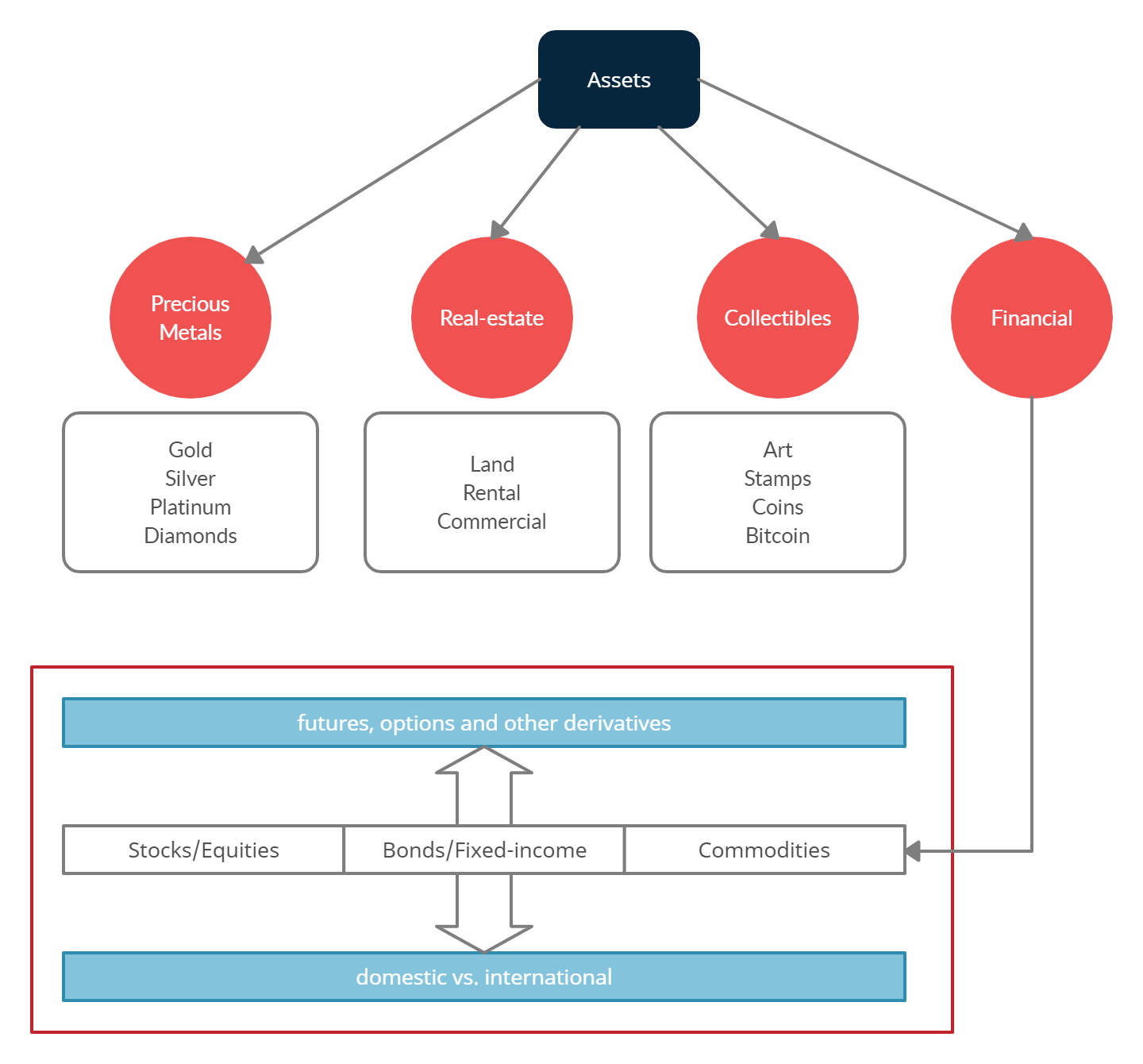

An asset class is a category of investment with particular risk and return characteristics. The following are some of the popular asset classes.

Fixed income instruments

Equity

Real estate

Commodities (precious metals)

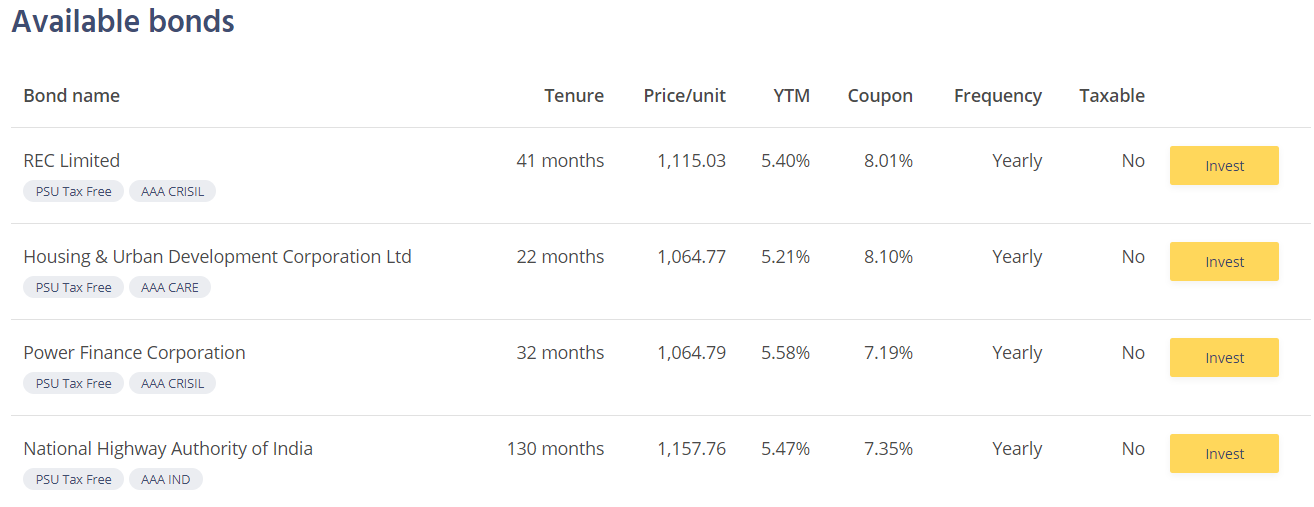

Fixed Income Instruments

These are investable instruments with minimal risk to the principle, and the return is paid as an interest to the investor based on the particular fixed-income instrument. The interest paid could be quarterly, semi-annual or annual intervals. At the end of the term of deposit, (also known as maturity period) the capital is returned to the investor.

Typical fixed income investment includes:

Fixed deposits offered by banks.

Bonds issued by the Government of India

Bonds issued by Government related agencies such as HUDCO, NHAI, etc

Bonds issued by corporate’s

As of June 2014, the typical return from a fixed income instrument varies between 8% and 11%.

Equity

Investment in Equities involves buying shares of publicly listed companies. The shares are traded on the Bombay Stock Exchange (BSE), and the National Stock Exchange (NSE).

When an investor invests in equity, unlike a fixed income instrument, there is no capital guarantee. However, as a trade-off, the returns from equity investment can be handsome. Indian Equities have generated returns close to 14% – 15% CAGR (compound annual growth rate) over the past 15 years.

Investing in some of the best and well run Indian companies has yielded over 20% CAGR in the long-term. Identifying such investment opportunities requires skill, hard work, and patience.

Taxation on Equity investments held for more than 365 days is taxed at 10%, if the gains are more than Rs 1 lakh starting from 1st April 2018(previously such investments were tax-free). This is comparatively a lower rate of tax than the other asset classes.

Real Estate Investment involves transacting (buying and selling) commercial and non-commercial land. Typical examples would include transacting in sites, apartments and commercial buildings. There are two income sources from real estate investments, namely – Rental income, and Capital appreciation of the investment amount.

The transaction procedure can be quite complex involving legal verification of documents. The cash outlay in real estate investment is usually quite large. There is no official metric to measure the returns generated by real estate. Hence it would be hard to comment on this.

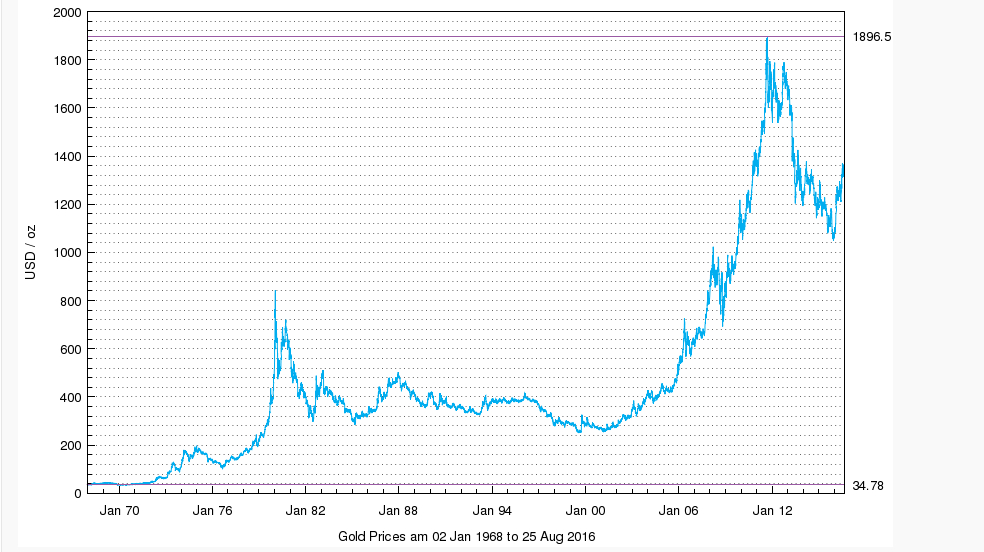

Investments in gold and silver are considered one of the most popular investment avenues. Gold and silver over a long-term period have appreciated. Investments in these metals have yielded a CAGR return of approximately 8% over the last 20 years. There are several ways to invest in gold and silver. One can choose to invest in the form of jewellery or Exchange Traded Funds (ETF).

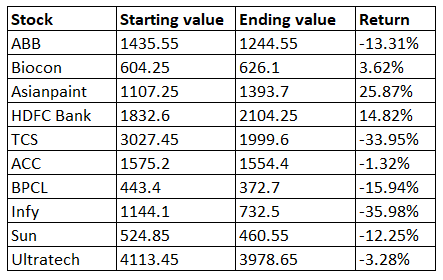

Going back to our initial example of investing the surplus cash it would be interesting to see how much one would have saved by the end of 20 years considering he can invest in any one – fixed income, equity or bullion.

By investing in fixed income at an average rate of 9% per annum, the corpus would have grown to Rs.3.3Crs.

Investing in equities at an average rate of 15% per annum, the corpus would have grown to Rs.5.4Crs.

Investing in bullion at an average rate of 8% per annum, the corpus would have grown to Rs.3.09Crs.

Clearly, equities tend to give you the best returns, especially when you have a multi-year investment perspective.

A note on investments

Investments optimally should have a strong mix of all asset classes. It is smart to diversify your investment among the various asset classes. The technique of allocating money across assets classes is termed as ‘Asset Allocation’.

For instance, a young professional may take a higher amount of risk given his age and years of investment available to him. Typically investors should allocate around 70% of their investable amount in Equity, 20% in Precious metals, and the rest in Fixed income investments.

Alongside the same rationale, a retired person could invest 80 per cent of his saving in fixed income, 10 per cent in equity markets and 10 per cent in precious metals. The ratio in which one allocates investments across asset classes depends on the investor’s risk appetite.

Investing is a great option, but before you venture into investments, it is good to be aware of the following…

Risk and Return go hand in hand. Higher the risk, higher the return. Lower the risk; lower is the return.

Investment in fixed income is a good option if you want to protect your principal amount. It is relatively less risky. However, you have the risk of losing money when you adjust the inflation return. Example – A fixed deposit which gives you 9% when the inflation is 10% means you are losing a net 1% per annum. Fixed-income investment is best suited for ultra risk-averse investors.

Investment in Equities is a great option. It is known to beat inflation over a long period of time. Historically equity investment has generated returns close to 14-15%. However, equity investments can be risky.

Real Estate investment requires a large outlay of cash and cannot be done with smaller amounts. Liquidity is another issue with real estate investment – you cannot buy or sell whenever you want. You always have to wait for the right time and the right buyer or seller to transact with you.

Gold and silver are relatively safer, but the historical return on such investment has not been very encouraging.

The corpus you intend to build at the end of the defined period is sensitive to the return rate the investment generates. A small variation to rate can have a big impact on the corpus.

Choose an instrument that best suits your risk and return appetite.

Equity should be a part of your investment if you want to beat the inflation in the long run

Investing in equities is an important investment that we make to generate inflation-beating returns. This was the conclusion we drew from the previous chapter. Having said that, how do we go about investing in equities? Clearly, before we dwell further into this topic, it is essential to understand the ecosystem in which equities operate.

Just like the way we go to the neighbourhood Kirana store or a supermarket to shop for our daily needs, similarly, we go to the stock market to shop (read as transact) for equity investments. The stock market is where everyone who wants to transact in shares goes to. Transact, in simple terms, means buying and selling. You can’t buy/sell shares of a public company like Infosys without transacting through the stock markets for all practical purposes.

The main purpose of the stock market is to help you facilitate your transactions. So if you are a buyer of a share, the stock market helps you meet the seller and vice versa.

Now unlike a supermarket, the stock market does not exist in a brick and mortar form. It exists in electronic form. You access the market electronically from your computer and go about conducting your transactions (buying and selling of shares).

It is also important to note that you can access the stock market via a registered intermediary called the stockbroker. We will discuss more the stockbrokers at a later point.

There are two main stock exchanges in India that make up the stock markets. They are the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE). Besides these two exchanges, there are many other regional stock exchanges like Bangalore Stock Exchange, Madras Stock Exchange that are more or less getting phased out and don’t really play any meaningful role anymore.

The stock market attracts individuals and corporations from diverse backgrounds. Anyone who transacts in the stock market is called a market participant. The market participant can be classified into various categories. Some of the categories of market participants are as follows:

Domestic Retail Participants – These are people like you and me transacting in markets

NRI’s and OCI – These are people of Indian origin but based outside India

Domestic Institutions – These are large corporate entities based in India. A classic example would be the LIC of India.

Domestic Asset Management Companies (AMC) – Typical participants in this category would be the mutual fund companies such as SBI Mutual Fund, DSP Black Rock, Fidelity Investments, HDFC AMC, etc.

Foreign Institutional Investors – Non-Indian corporate entities. These could be foreign asset management companies, hedge funds, and other investors.

Now, irrespective of the category of market participant, everyone’s agenda is the same – to make profitable transactions. More bluntly put – to make money.

When money is involved, human emotions in the form of greed and fear run high. One can easily fall prey to these emotions and get involved in unfair practices. India has its fair share of such twisted practices, thanks to Harshad Mehta’s operations and the like.

Given this, the stock markets need someone who can set the game rules (commonly referred to as regulation and compliance) and ensure that people adhere to these regulations and compliance thereby making the markets a level playing field for everyone.

In India, the stock market regulator is called The Securities and Exchange Board of India, often referred to as SEBI. The objective of SEBI is to promote the development of stock exchanges, protect the interest of retail investors, and regulate market participants and financial intermediaries’ activities. In general, SEBI ensures:

The stock exchanges (BSE and NSE) conducts its business fairly

Stockbrokers and sub-brokers conduct their business fairly

Participants don’t get involved in unfair practices

Corporate’s don’t use the markets to unduly benefit themselves (Example – Satyam Computers)

Small retail investors interests are protected

Large investors with huge cash pile should not manipulate the markets

Overall development of markets

Given the above objectives, it becomes imperative for SEBI to regulate the following entities. All the entities mentioned below are directly involved in the stock markets. Malpractice by anyone of the following entities can disrupt what is otherwise a harmonious market in India.

SEBI has prescribed a set of rules and regulations to each one of these entities. The entity should operate within the legal framework as prescribed by SEBI. The specific rules applicable to a specific entity are made available by SEBI on their website. They are published under the ‘Legal Framework’ section of their site.

Entity

Example of companies

What do they do?

In simpler words

Credit Rating Agency (CRA)

CRISIL, ICRA, CARE

They rate the creditworthiness of corporate and governments

If a corporate or Govt entity wants to avail the loan, CRA checks if the entity is worthy of giving a loan

Debenture Trustees

Almost all banks in India

Act as a trustee to corporate debenture

When companies want to raise a loan, they can issue debenture against which they promise to pay interest. The public can subscribe to these debentures. A Debenture Trustee ensures that the

debenture obligation is honoured

Depositories

NSDL and CDSL

Safekeeping, reporting and settlement of clients securities

Acts like a vault for the shares that you buy. The depositories hold your shares and facilitate the exchange of your securities. When you buy shares these shares sit in your Depositary account usually referred to as the DEMAT account. This is maintained electronically by only two companies in India

Depository Participant (DP)

Most of the banks and few stockbrokers

Act as an agent to the two depositories

You cannot directly interact with NSDL or CDSL. You need to liaison with a DP to open and maintain your DEMAT account

Foreign Institutional Investors

Foreign corporate, funds and individuals

Make investments in India

These are foreign entities with interest to invest in India. They usually transact in large amounts of money, and hence their activity in the markets have an impact in terms of market sentiment

Merchant Bankers

Karvy, Axis Bank, Edelweiss Capital

Help companies raise money in the primary markets

If a company plans to raise money by floating an IPO, then merchant bankers are the ones who help companies with the IPO process

Asset Management Companies

(AMC)

HDFC AMC, Reliance Capital, SBI Capital

Offer Mutual Fund Schemes

An AMC collects money from the public, puts that money in a single account, and then invests that money in markets intending to make the investments grow and generate wealth.

Portfolio Managers/

Portfolio Management System

(PMS)

Religare Wealth Management, Parag Parikh PMS

Offer PMS schemes

They work similarly to a mutual fund except in a PMS; you have to invest a minimum of Rs.25,00,000; however, there is no such cap in a mutual fund.

Stock Brokers and Sub Brokers

Zerodha, Sharekhan, ICICI Direct

Act as an intermediary between an investor and the stock exchange

Whenever you want to buy or sell shares from the stock exchange, you have to do so through registered stock brokers. A sub-broker is like an agent to a stockbroker.

The stock market is the place to go to if you want to transact in equities.

Stock markets exist electronically and can be accessed through a stockbroker.

There are many different kinds of market participants operating in the stock markets.

Every entity operating in the market has to be regulated, and they can operate only within the framework as prescribed by the regulator.

SEBI is the regulator of the securities market in India. They set the legal framework and regulate all entities interested in operating in the market.

Most importantly you need to remember that SEBI is aware of what you are doing and they can flag you down if you are upto something fishy in the markets!

From the time you access the market – let’s say, to buy a stock till the stocks come and hit your DEMAT account, many corporate entities are actively involved in making this work for you. These entities play their role quietly behind the scene, always complying with the rules laid out by SEBI and ensure an effortless and smooth experience for your transactions in the stock market. These entities are generally referred to as the Financial Intermediaries.

Together, these financial intermediaries, interdependent of one another, create an ecosystem in which the financial markets exist. This chapter will help you get an overview of what these financial intermediaries are and the services they offer.

3.2 The Stock Broker

The stockbroker is probably one of the most important financial intermediaries that you need to know. A stockbroker is a corporate entity, registered as a trading member with the stock exchange and holds a stockbroking license. They operate under the guidelines prescribed by SEBI.

A stockbroker is your gateway to stock exchanges. First, you need to open something called a ‘Trading Account’ with a broker who meets your requirements. Your requirement could be as simple as the proximity between the broker’s office and your house. Simultaneously, it can be as complicated as identifying a broker who can provide you with a single platform using which you can transact across multiple exchanges across the world. At a later point, we will discuss what these requirements could be and how to choose the right broker.

A trading account lets you carry financial transactions in the market. A trading account is an account with the broker, which lets the investor buy/sell securities.

So assuming you have a trading account – whenever you want to transact in the markets, you need to interact with your broker. There are a few standard ways through which you can interact with your broker.

You can go to the broker’s office and meet the dealer in the broker’s office and tell him what you wish to do. A dealer is an executive at the stock broker’s office who carries out these transactions on your behalf.

You can make a telephone call to your broker, identify yourself with your client code (account code) and place an order for your transaction. The dealer at the other end will execute the order for you and confirm the status of the same while you are still on the call.

Do it yourself – this is perhaps the most popular way of transacting in the markets. The broker gives you access to the market through software called ‘Trading Terminal’. After you log in to the trading terminal, you can view live price quotes from the market and place orders yourself.

The basic services provided by the brokers include…

Give you access to markets and letting you transact

Give you margins for trading – We will discuss this point at a later stage.

Provide support – Dealing support if you have to call and trade. Software support if you have issues with the trading terminal

Issue contract notes for the transactions – A contract note is a written confirmation detailing the transactions you have carried out during the day.

Facilitate the fund transfer between your trading and bank account

Provide you with a back-office login – using which you can see the summary of your account

The broker charges a fee for the services he provides called the ‘brokerage charge’ or just brokerage. The brokerage rates vary, and it’s upto you to find a broker who strikes a balance between the fee he collects versus the services he provides.

When you buy a property, the only way to identify and claim that you actually own the property is by producing the property papers. Hence it becomes essential to store the property papers in a safe and secure place.

Likewise, when you buy a share (a share represents part ownership in a company) the only way to claim your ownership is by producing your share certificate. A share certificate is nothing but a piece of document entitling you as the owner of the shares in a company.

Before 1996 the share certificate was in paper format; however post 1996, the share certificates were converted to digital form. Converting a paper format share certificate into a digital format share certificate is called “Dematerialization” often abbreviated as DEMAT.

The share certificate in DEMAT format has to be stored digitally. The storage place for the digital share certificate is the ‘DEMAT Account’. A Depository is a financial intermediary which offers the service of the Demat account. A DEMAT account in your name will have all the shares in the electronic format you bought. Think of the DEMAT account as a digital vault for your shares.

As you may have guessed, your broker’s trading account and the DEMAT account from the Depository are interlinked.

For example, if your idea is to buy Infosys shares, then all you need to do is open your trading account, look for Infosys’ prices, and buy it. Once the transaction is complete, the role of your trading account is done. After you buy, the shares of Infosys will automatically come and sit in your DEMAT account.

Likewise, when you wish to sell Infosys shares, all you have to do is open your trading account and sell the stock. This takes care of the transaction part…however in the backend, the shares which are sitting in your DEMAT account will get debited, and the shares move out of your DEMAT account.

At present, only two depositaries are offering you DEMAT account services. They are The National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited. There is virtually no difference between the two, and both of them operate under strict SEBI regulations.

Just like the way you cannot walk into National Stock Exchange’s office to open a trading account, you cannot walk into a Depository to open a DEMAT account. To open a DEMAT account, you need to liaison with a Depository Participant (DP). A DP helps you set up your DEMAT account with a Depository. A DP acts as an agent to the Depository. Needless to say, even the DP is governed by the regulations laid out by the SEBI.

Banks play a very straightforward role in the market ecosystem. They help in facilitating the fund transfer from your bank account to your trading account. You cannot transfer money from a bank account that is not in your name.

You can link multiple bank accounts to your trading through which you can transfer funds and trade. At Zerodha, you can add 1 primary bank account and up to 2 secondary bank accounts. You can use all the bank accounts to add funds, but withdrawals are only processed to the primary bank account. Also, dividend payments, money from buybacks will be sent to the primary bank account. The primary bank account is connected to your trading account and with the Depository and the Registrar and transfer agents (RTA).

At this stage, you must have realized that the three financial intermediaries operate via three different accounts – trading account, DEMAT account and Bank account. All three accounts operate electronically and are interlinked, giving you a very seamless experience.

NSCCL – National Security Clearing Corporation Ltd and Indian Clearing Corporation are wholly owned subsidiaries of National Stock Exchange and Bombay Stock Exchange.

The job of the clearing corporation is to ensure guaranteed settlement of your trades/transactions. For example, if you were to buy 1 share of Biocon at Rs.446 per share, there must be someone who has sold that 1 share to you at Rs.446. For this transaction, you will be debited Rs.446 from your trading account, and someone must be credited that Rs.446 toward the sale of Biocon. In a typical transaction like this, the clearing corporation’s role is to ensure the following:

a) Identify the buyer and seller and match the debit and credit process

b) Ensure no defaults – The clearing corporation also ensures there are no defaults by either party. For instance, after selling the shares, the seller should not be in a position to back out, thereby defaulting in his transaction.

For all practical purposes, it’s ok not to know much about NSCCL or ICCL simply because, you as a trader or investor would not be interacting with these agencies directly. You need to be aware that certain professional institutions are heavily regulated and work towards a smooth settlement and efficient clearing activity.

The market ecosystem is built by a cluster of financial intermediaries, each offering services unique to the functioning of markets.

A stockbroker is your access to markets, so make sure you choose a broker that matches your requirements, and services well.

A stockbroker provides you with a trading account which is used for all market-related transactions (buying and selling of financial instruments like shares)

A Depository is a corporate entity which holds the shares in electronic form, against your name, in your account. Your account with the depository is called the ‘DEMAT’ account.

There are only two depositories in India – NSDL and CDSL.

To open a DEMAT account with one of the depositaries, you need to liaison with a Depository Participant (DP). A DP functions as an agent to the Depository

A clearing corporation works towards clearing and settling of trades executed by you.

The initial three chapters have set the background on some of the basic market concepts you need to know. It becomes imperative to address a fundamental question at this stage – Why do companies go public?

A good understanding of this topic lays down a sound foundation for all future topics. We will learn new financial concepts during the course of this chapter.

Before we jump ahead to seek an answer as to why companies go public, let us spend some time figuring out a more basic concept – the origins of a typical business. To understand this concept better, we will build a tangible story around it. Let us split this story into several scenes to get a clear understanding of how the business and the funding environment evolve.

Scene 1 – The Angels

Imagine a budding entrepreneur with a brilliant business idea – to manufacture highly fashionable, organic cotton t-shirts. The designs are unique, has attractive price points, and the best quality cotton is used to make these t-shirts. He is confident that the business will be successful and is enthusiastic about launching the idea into a business.

As a typical entrepreneur, he is likely to be hit by the typical problem – where would he get the money to fund the idea? Assuming the entrepreneur has no business background, he will not attract any serious investor at the initial stage. Chances are, he would approach his family and friends to pitch the idea and raise some money. He could approach the bank for a loan, but this would not be the best option.

Let us assume that he pools in his own money and convinces two of his good friends to invest in his business. These two friends are investing in the pre-revenue stage and taking a blind bet on the entrepreneur called the Angel investors. Please note, the money from the angels is not a loan; it is actually an investment made by them.

So let us imagine that the promoter, along with the angels, raises INR 5 Crore in the capital. This initial money that he gets to kick start his business is called ‘The Seed Fund’. It is important to note that the seed fund will not sit in the entrepreneur’s (also called the promoter) personal bank account but instead sits in its bank account. Once the seed capital hits the company’s bank account, the money will be referred to as the company’s initial share capital.

In return for the initial seed investment, the original three (promoter plus 2 angels) will be issued share certificates of the company which entitles them to the company.

The only asset that the company has at this stage is the cash of INR 5 Crs, the company’s value is also INR 5 Crs. This is called the company’s valuation.

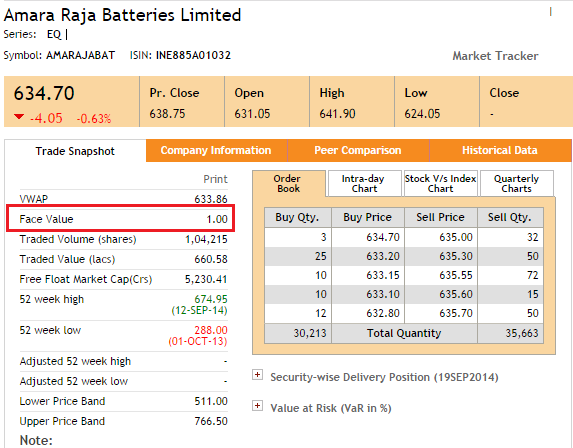

Issuing shares is quite simple; the company assumes that each share is worth Rs.10 and because there is Rs.5 crore as share capital, there have to be 50 lakh shares with each share worth Rs.10. In this context, Rs.10 is called the ‘Face value’ (FV) of the share. The face value could be any number. If the FV is Rs.5, then the number of shares would be 1 crore, so on and so forth.

A total of 50 lakh shares is called the Authorized shares of the company. These shares have to be allotted amongst the promoter, and two angels plus the company has to retain some amount of shares with itself to be issued in the future.

So let us assume the promoter retains 40% of the shares, and the two angels get 5% each, and the company retains 50% of the shares. Since the promoter and two angels own 50% of the shares, this allotted portion is called Issued shares.

The shareholding pattern of this company would look something like this:

Sl No

Name of Share Holder

No of Shares

%Holding

1

Promoter

2,000,000

40%

2

Angel 1

250,000

05%

3

Angel 2

250,000

05%

Total

2,500,000

50%

Please note the company retains the balance of 50% of the shares totalling 2,500,000 equity shares. These shares are authorized but not allotted.

Now backed by a good company structure and a healthy seed fund, the promoter kick starts his business operations. He wants to move cautiously. Hence he decides to open just one small manufacturing unit and one store to retail his product.

Scene 2 – The Venture Capitalist

His hard work pays off, and the business starts to pick up. At the end of the first two years of operations, the company starts to break even. The promoter is now no longer a rookie business owner. Instead, he is more knowledgeable about his own business and of course, more confident.

Backed by his confidence, the promoter now wants to expand his business by adding 1 more manufacturing unit and a few additional retail stores in the city. He chalks out the plan and figures out that the fresh investment needed for his business expansion is INR 7 Crs.

He is now in a better situation when compared to where he was two years ago. The big difference is the fact that his business is generating revenues. The healthy inflow of revenue validates the business and its offerings. He is now in a situation where he can access reasonably savvy investors for investing in his business. Let us assume he meets one such professional investor who agrees to give him 7 Crs for a 14% stake in his company.

The investor who typically invests in such an early stage of business is called a Venture Capitalist (VC), and the money that the business gets at this stage is called Series A funding.

After the company agrees to allot 14% to the VC from the authorized capital, the shareholding pattern looks like this:

Sl No

Name of Share Holder

No of Shares

%Holding

1

Promoter

2,000,000

40%

2

Angel 1

250,000

05%

3

Angel 2

250,000

05%

4

Venture Capitalist

700,000

14%

Total

3,200,000

64%

Note, the balance 36% of shares is still retained within the company and has not been issued.

With the VC’s money coming into the business, an exciting development has taken place. The VC values the entire business at INR 50 Crs by valuing his 14% stake in the company at INR 7Crs. With the initial valuation of 5Crs, there is a 10 fold increase in the company’s valuation. This is what a good business plan, validated by a healthy revenue stream, can do to businesses. It works as a perfect recipe for wealth creation.

With the valuations going up, the investments made by the initial investors will have an impact. The following table summarizes the same…

Sl No

Name of Share Holder

Initial Shareholding

Initial Valuation

Shareholding after 2 Yrs

Valuation after 2 Yrs

Wealth Created

1

Promoter

40%

2 Cr

40%

20 Cr

10 times

2

Angel 1

05%

25 Lakhs

05%

2.5 Cr

10 times

3

Angel 2

05%

25 Lakhs

05%

2.5 Cr

10 times

4

Venture Capitalist

0%

-NA-

14%

07 Cr

-NA-

Total

50%

2.5 Cr

64%

32 Cr

Going forward with our story, the promoter now has the additional capital he requires for the business. The company gets an additional manufacturing unit and a few more retail outlets in the city as planned. Things are going great; the popularity of the product grows, translating into higher revenues. The management team gets more professional, thereby increasing the operational efficiency, which translates to better profits.

Scene 3 – The Banker

Three more years pass by, and the company is phenomenally successful. The company decides to have a retail presence in at least 3 more cities. To back the retail presence across three cities, the company also plans to increase the production capacity and hire more resources. Whenever a company plans such expenditure to improve the overall business, the expenditure is called ‘Capital Expenditure’ or simply ‘CAPEX’.

The management estimates 40Crs towards their CAPEX requirements. How does the company get this money or in other words, how can the company fund its CAPEX requirements?

There are few options with the company to raise the required funds for their CAPEX:

The company has made some profits over the last few years; a part of the CAPEX requirement can be funded through the profits. This is also called funding through internal accruals.

The company can approach another VC and raise another round of VC funding by allotting shares from the authorized capital – this is called Series B funding.

The company can approach a bank and seek a loan. The bank would be happy to tender this loan as the company has been doing fairly well. The loan is also called ‘Debt.’

The company decides to exercise all three options at its disposal to raise funds for Capex. It ploughs 15Crs from internal accruals, plans a series B – divests 5% equity for a consideration of 10Crs from another VC and raises 15Crs debt from the banker.

Note, with 10Crs coming in for 5%, the company’s valuation now stands at 200 Crs. Of course, this may seem a bit exaggerated, but then the whole purpose of this story is to drive across the concept!

The shareholding and valuation look something like this:

Sl No

Name of Share Holder

No of Shares

%Holding

Valuation

1

Promoter

2,000,000

40%

80 Cr

2

Angel 1

250,000

05%

10 Cr

3

Angel 2

250,000

05%

10 Cr

4

VC Series A

700,000

14%

28 Cr

5

VC Series B

250,000

05%

10 Cr

Note, the company still has 31% of shares not allotted to shareholders now being valued at 62 Crs. Also, I would encourage you to think about the wealth that has been created over the years. This is exactly what happens to entrepreneurs with great business ideas and a highly competent management team.

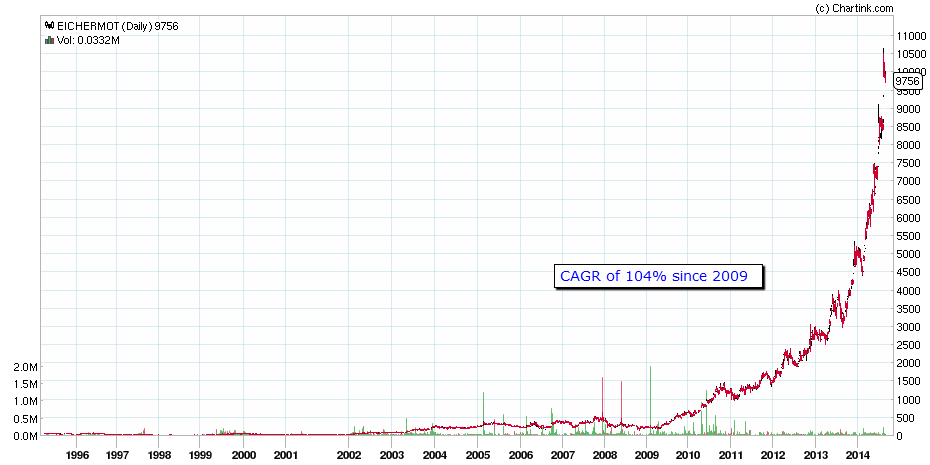

Classic real-world examples of such wealth creation stories would be Infosys, Page Industries, Eicher Motors, Titan Industries, and the international space one could think of Google, Facebook, Twitter, Whatsapp, etc.

Scene 4 – The Private Equity

A few years pass by, and the company’s success continues to shine on. With the growing success of this 8-year-old, 200 Cr Company, the ambitions are also growing. The company decides to raise the bar and branch out across the country. They also decide to diversify the company by manufacturing and retailing fashion accessories, designer cosmetics and perfumes.

The CAPEX requirement for the new ambition is now pegged at 60 Crs. The company does not want to raise money through debt because of the interest rate burden, also called the financecharges, which would eat away the company’s profits.

They decide to allot shares from the authorized capital for a Series C funding. They cannot approach a typical VC because VC funding is usually small and runs into a few crores. This is when a Private Equity (PE) investor comes into the picture.

PE investors are quite savvy. They are highly qualified and have an excellent professional background. They invest large amounts of money to provide the capital for constructive use and place their own people on the board of the investee company to ensure the company steers in the required direction.

Assuming they pick up a 15% stake for a consideration of 60Crs, they are now valuing the company at 400Crs. Let’s have a quick look at the shareholding and valuations:

Sl No

Name of Share Holder

No of Shares

%Holding

Valuation (in Crs)

1

Promoter

2,000,000

40%

160

2

Angel 1

250,000

05%

20

3

Angel 2

250,000

05%

20

4

VC Series A

700,000

14%

56

5

VC Series B

250,000

05%

20

6

PE Series C

7,50,000

15%

60

Total

4,450,000

84%

336

Please note, the company has retained a 16% stake which has not been allotted to any shareholder. This portion is valued at 64 Crs.

Usually, when a PE invests, they invest intending to fund large CAPEX requirements. Besides, they do not invest in the early stage of a business; instead, they prefer to invest in companies that already have a revenue stream, and are in operation for a few years. Deploying the PE capital and utilizing the capital for the CAPEX requirements takes up a few years.

Scene 5 – The IPO

5 years after the PE investment, the company has progressed really well. They have successfully diversified their product portfolio and have a presence across all the country’s major cities. Revenues are good, profitability is stable, and the investors are happy. The promoter, however, does not want to settle in for just this.

The promoter now aspires to go international! He wants his brand to be available across all the major international cities; he wants at least two outlets in each major city across the world.

This means the company needs to invest in market research to understand what people like in other countries, invest in people, and increase manufacturing capacities. Besides they also need to invest in real estate space across the world.

This time around the CAPEX requirement is huge, and the management estimates this at 200 Crs. The company has few options to fund the CAPEX requirement.

Fund Capex from internal accruals

Raise Series D from another PE fund

Raise debt from bankers

Float a bond (this is another form of raising debt)

File for an Initial Public Offer (IPO) by allotting shares from authorized capital

A combination of all the above

For convenience, let us assume the company decides to fund the CAPEX partly through internal accruals and files for an IPO. When a company files for an IPO, they have to offer their shares to the general public. The general public will subscribe to the shares (i.e. if they want to) by paying a certain price. Now, because the company is offering the shares for the first time to the public, it is called the “Initial Public Offer’.

We are now at a very crucial juncture, where a few questions need to be answered.

Why did the company decide to file for an IPO? In general, why do companies go public?

Why did they not file for the IPO when they were in Series A, B and C situation?

What would happen to the existing shareholders after the IPO?

What does the general public look for before they subscribe to the IPO?

How does the IPO process evolve?

Which of the financial intermediaries involved in the IPO markets?

What happens after the company goes public?

In the following chapter, we will address each of the above questions plus more, and we will also give you more insights into the IPO Market. For now, hopefully, you should have developed a sense of how a successful company evolves before they come out to the public to offer their shares.

This chapter aims to give you a sense of completeness when one thinks about an IPO.

Before understanding why companies go public, it is important to understand the origin of business.

The people who invest in your business in the pre-revenue stage are called Angel Investors.

Angel investors take the maximum risk. They take in as much risk as the promoter.

The money that angels give to start the business is called the seed fund.

Angel’s invest relatively a small amount of capital

Valuation of a company simply signifies how much the company is valued at. When one values the company, they consider the company’s assets and liabilities.

Face value is simply a denominator to indicate how much one share is originally worth.

Authorized shares of the company are the total number of shares that are available with the company.

The shares distributed from the authorized shares are called the issued shares. Issued shares are always a subset of authorized shares.

The shareholding pattern of a company tells us who owns how much stake in the company.

Venture Capitalists invest at an early stage in business; they do not risk Angel investors. The quantum of investments by a VC is usually somewhere in between an angel and private equity investment.

The money the company spends on business expansion is called capital expenditure or CAPEX

Series A, B, and C, etc., are all funding that the company seeks as they start evolving. Usually higher the series, higher is the investment required.

Beyond a certain size, VCs cannot invest, and hence the company seeking investments will have to approach Private Equity firms.

PE firms invest large sums of money, and they usually invest at a slightly more mature stage of the business.

In terms of risk, PE’s have a lower risk appetite as compared to VC or angels.

Typical PE investors would like to deploy their own people on the investee company’s board to ensure business moves in the right direction.

The valuation of the company increases as and when the business, revenues and profitability increases.

An IPO is a process using which a company can raise fund. The funds raised can be for any valid reason – for CAPEX, restructuring debt, rewarding shareholders, etc

The previous chapter gave us an understanding of how a company evolved right from the idea generation stage to all the way until it decides to file for an IPO. The idea behind creating the fictional story in the previous chapter was to give you a sense of how a business matures over time. The emphasis obviously was on the different stages of business and funding options available at various stages of business. The previous chapter gives you a perspective of what a company would have gone through before it comes out to the public to offer its shares.

This is extremely important to know because the IPO market, also called the Primary market sometimes attracts companies offering their shares to the public without actually going through a healthy round of funding in the past. A few rounds of funding by credible VC and PE firms validate the quality of the business and its promoters. Of course, you need to treat this with a pinch of salt but nevertheless it acts as an indicator to identify well run companies.

We closed the previous chapter with a few critical questions. One of which – Why did the company decide to file for an IPO, and in general why do companies go public?

When a company decides to file for an IPO, invariably the main reason is to raise funds to fuel their CAPEX requirement. The promoter has 3 advantages by taking his company public:

He is raising funds to meet CAPEX requirement

He is avoiding the need to raise debt which means he does not have to pay finance charges which translates to better profitability

Whenever you buy a share of a company, you are in essence taking the same amount of risk as the promoter is taking. Needless to say, the proportion of the risk and its impact will depend on the number of shares you hold. Nonetheless, whether you like it or not, when you buy shares you also buy risk. So when the company goes public, the promoter is actually spreading his risk amongst a large group of people.

There are other advantages as well in going for an IPO…

Provide an exit for early investors – Once the company goes public, the shares of the company start trading publicly. Any existing shareholder of the company – could be promoters, angel investors, venture capitalists, PE funds; can use this opportunity to sell their shares in the open market. By selling their shares, they get an exit on their initial investment in the company. They can also choose to sell their shares in smaller chunks if they wish.

Reward employees –Employees working for the company would have shares allotted to them as an incentive. This sort of arrangement between the employee and the company is called the “Employee Stock Option”. The shares are allotted at a discount to the employees. Once the company goes public, the employees stand a chance to see capital appreciation in the shares. Few examples where the employee benefited from ESOP would be Google, Infosys, Twitter, Facebook, etc

Improve visibility – Going public definitely increases visibility as the company has a status of being publicly held and traded. There is a greater chance of people’s interest in the company, consequently creating a positive impact on its growth.

So let’s just build on our fictional business story from the previous chapter a little further and figure out the IPO details of this company.

If you recollect, the company requires 200 Crs to fund their CAPEX and the management had decided to fund this partly by internal accrual and partly by filing for an IPO.

Do recollect that the company still has 16% of authorized capital translating to 800,000 shares which are not allotted. The last valuation of these shares when the PE firm invested in Series B was 64Crs. The company has progressed really well ever since the PE firm has invested and naturally the valuation of these shares would have gone up.

For the sake of simplicity, let us assume the company is now valuing the 16% shares anywhere between 125 Crs to 150 Crs. This translates to a per-share value, anywhere between Rs.1562 to Rs.1875/-…(125Crs/8lakh).

So if the company puts 16% on the block to the public, they are likely to raise anywhere between 125 to 150 Crs. The remainder has to come from internal accruals. So naturally, the more money they raise, the better it is for the company.

Having decided to go public, the company must now do a series of things to ensure a successful initial public offering. The first and foremost step would be to appoint a merchant banker. Merchant bankers are also called Book Running Lead Managers (BRLM)/Lead Manager (LM). The job of a merchant banker is to assist the company with various aspects of the IPO process including:

Conduct due diligence on the company filing for an IPO, ensure their legal compliance and also issue a due diligence certificate

Should work closely with the company and prepare their listing documents including Draft Red Herring Prospectus (DRHP). We will discuss this in a bit more detail at a later stage

Underwrite shares – By underwriting shares, merchant bankers essentially agree to buy all or part of the IPO shares and resell the same to the public

Help the company arrive at the price band for the IPO. A price band is the lower and upper limit of the share price within which the company will go public. In the case of our example, the price band will be Rs.1562/- and Rs.1875/-

Help the company with the roadshows – This is like a promotional/marketing activity for the company’s IPO

Appointment of other intermediaries namely, registrars, bankers, advertising agencies, etc. The Lead manager also makes various marketing strategies for the issue

Once the company partners with the merchant banker, they will work towards taking the company public.

Needless to say, each and every step involved in the IPO sequence has to happen under the SEBI guidelines. In general, the following are the sequence of steps involved.

Appoint a merchant banker. In case of a large public issue, the company can appoint more than 1 merchant banker

Apply to SEBI with a registration statement – The registration statement contains details on what the company does, why the company plans to go public and the financial health of the company

Getting a nod from SEBI – Once SEBI receives the registration statement, SEBI takes a call on whether to issue a go-ahead or a ‘no go’ to the IPO

DRHP – If the company gets the initial SEBI nod, then the company needs to prepare the DRHP. A DRHP is a document that gets circulated to the public. Along with a lot of information, DRHP should contain the following details:

The estimated size of the IPO

The estimated number of shares being offered to the public

Why the company wants to go public and how does the company plan to utilize the funds along with the timeline projection of fund utilization

Business description including the revenue model, expenditure details

Complete financial statements

Management Discussion and Analysis – how the company perceives future business operations to emerge

Risks involved in the business

Management details and their background

Market the IPO – This would involve TV and print advertisements in order to build awareness about the company and its IPO offering. This process is also called the IPO roadshow

Fix the price band – Decide the price band between which the company would like to go public. Of course, this can’t be way off the general perception. If it is, then the public will not subscribe for the IPO

Book Building – Once the roadshow is done and the price band fixed the company now has to officially open the window during which the public can subscribe for shares. For example, if the price band is between Rs.100 and Rs.120, then the public can actually choose a price they think is fair enough for the IPO issue. The process of collecting all these price points along with the respective quantities is called Book Building. Book building is perceived as an effective price discovery method

Closure – After the book building window is closed (generally open for few days) then the price point at which the issue gets listed is decided. This price point is usually the price at which maximum bids have been received.

Listing Day – This is the day when the company actually gets listed on the stock exchange. The listing price is the price decided based on market demand and supply on that day and the stock is listed at a premium, par or discount of the cut-off price

During the bidding process (also called the date of issue) investors can bid for shares at a particular price within the specified price band. This whole system around the date of the issue where one bids for shares, is referred to as the Primary Market. The moment the stock gets listed and debuts on the stock exchange, the stock starts to trade publicly. This is called the secondary market.

Once the stock transitions from primary markets to secondary markets, the stock gets traded daily on the stock exchange. People start buying and selling stocks regularly.

Why do people trade? Why does the stock price fluctuate? Well, we will answer all these questions and more in the subsequent chapters.

Before we wrap up the chapter on IPO’s let us review a few important IPO jargons.

Under subscription – Let’s say the company wants to offer 100,000 shares to the public. During the book-building process, it is discovered that only 90,000 bids were received, then the issue is said to be under subscribed. This is not a great situation to be in as it indicates negative public sentiment

Oversubscription – If there are 200,000 bids for 100,000 shares on offer then the issue is said to be oversubscribed 2 times (2x)

Green Shoe Option – Part of the underwriting agreement which allows the issuer to authorize additional shares (typically 15 percent) to be distributed in the event of oversubscription. This is also called the overallotment option

Fixed Price IPO –Sometimes the companies fix the price of the IPO and do not opt for a price band. Such issues are called fixed price IPO

Price Band and Cut off price –Price band is a price range between which the stock gets listed. For example, if the price band is between Rs.100 and Rs.130, then the issue can list within the range. Let’s says it gets listed at 125, then 125 is called the cut off price.

Having understood the IPO process and what really goes behind the company’s transition from primary to secondary market we are now set to explore the stock markets a step further.

By virtue of being a public company, the company is now liable to disclose all information related to the company to the public. The shares of a public limited company are traded on the stock exchanges on a daily basis.

There are few reasons why market participants trade stocks. We will explore these reasons in this chapter.

Like we discussed in chapter 2, the stock market is an electronic market place. Buyers and sellers meet and trade their point of view.

For example, consider the current situation of Infosys. At the time of writing this, Infosys is facing a succession issue, and most of its senior level management personnel are quitting the company for internal reasons. It seems like the leadership vacuum is weighing down the company’s reputation heavily. As a result, the stock price dropped to Rs.3,000 all the way from Rs.3,500. Whenever there are new reports regarding Infosys management change, the stock prices react to it.

Assume there are two traders – T1 and T2.

T1’s point of view on Infosys – The stock price is likely to go down further because the company will find it challenging to find a new CEO.

If T1 trades as per his point of view, he should be a seller of the Infosys stock.

T2, however views the same situation in a different light and therefore has a different point of view – According to him, the stock price of Infosys has over reacted to the succession issue and soon the company will find a great leader, after whose appointment the stock price will move upwards.

If T2 trades as per his point of view, he should be a buyer of the Infosys stock.

So at, Rs.3, 000 T1 will be a seller, and T2 will be a buyer in Infosys.

Now both T1 and T2 will place orders to sell and buy the stocks respectively through their respective stock brokers. The stock broker, obviously routes it to the stock exchange.

The stock exchange has to ensure that these two orders are matched, and the trade gets executed. This is the primary job of the stock market – to create a market place for the buyer and seller.

The stock market is a place where market participants can access any publicly listed company and trade from their point of view, as long as there are other participants who have an opposing point of view. After all, different opinions are what make a market.

Let us continue with the Infosys example to understand how stocks really move. Imagine you are a market participant tracking Infosys.

It is 10:00 AM on 11th June 2014 ,and the price of Infosys is 3000. The management makes a statement to the press that they have managed to find a new CEO who is expected to steer the company to greater heights. They are confident on his capabilities and they are sure that the new CEO will deliver much more than what is expected out of him.

Two questions –

How will the stock price of Infosys react to this news?

If you were to place a trade on Infosys, what would it be? Would be a buy or a sell?

The answer to the first question is quite simple, the stock price will move up.

Infosys had a leadership issue, and the company has fixed it. When positive announcements are made market participants tend to buy the stock at any given price and this cascades into a stock price rally.

Let me illustrate this further :

Sl No

Time

Last Traded Price

What price the seller wants

What does the buyer do?

New Last Trade Price

01

10:00

3000

3002

He buys

3002

02

10:01

3002

3006

He buys

3006

03

10:03

3006

3011

He buys

3011

04

10:05

3011

3016

He buys

3016

Notice, whatever prices the seller wants the buyer is willing to pay for it. This buyer-seller reaction tends to push the share price higher.

So as you can see, the stock price jumped 16 Rupees in a matter of 5 minutes. Though this is a fictional situation, it is a very realistic, and typical behavior of stocks. The stocks price tends to go up when the news is good or expected to be good.

In this particular case, the stock moves up because of two reasons. One, the leadership issue has been fixed, and two, there is also an expectation that the new CEO will steer the company to greater heights.

The answer to the second question is now quite simple; you buy Infosys stocks considering the fact that there is good news surrounding the stock.

Now, moving forward in the same day, at 12:30 PM ‘The National Association of Software & Services company’, popularly abbreviated as NASSCOM makes a statement. For those who are not aware, NASSCOM is a trade association of Indian IT companies. NASSCOM is considered to be a very powerful organization and whatever they say has an impact on the IT industry.

The NASSCOM makes a statement stating that the customer’s IT budget seems to have come down by 15%, and this could have an impact on the industry going forward.

By 12:30 PM let us assume Infosys is trading at 3030. Few questions for you..

How does this new information impact Infosys?

If you were to initiate a new trade with this information what would it be?

What would happen to the other IT stocks in the market?

The answers to the above questions are quite simple. Before we start answering these questions, let us analyze NASSCOM’s statement in a bit more detail.

NASSCOM says that the customer’s IT budget is likely to shrink by 15%. This means the revenues and the profits of IT companies are most likely to go down soon. This is not great news for the IT industry.

Let us now try and answer the above questions..

Infosys being a leading IT major in the country will react to this news. The reaction could be mixed one because earlier during the day there was good news specific to Infosys. However a 15% decline in revenue is a serious matter and hence Infosys stocks are likely to trade lower

At 3030, if one were to initiate a new trade based on the new information, it would be a sell on Infosys

The information released by NASSCOM is applicable to the entire IT stocks and not just Infosys. Hence all IT companies are likely to witness a selling pressure.

So as you notice, market participants react to news and events and their reaction translates to price movements! This is what makes the stocks move.

At this stage you may have a very practical and valid question brewing in your mind. You may be thinking what if there is no news today about a particular company? Will the stock price stay flat and not move at all?

Well, the answer is both yes and no, and it really depends on the company in focus.

For example let us assume there is absolutely no news concerning two different companies..

Reliance Industries Limited

Shree Lakshmi Sugar Mills

As we all know, Reliance is one the largest companies in the country and regardless of whether there is news or not, market participants would like to buy or sell the company’s shares and therefore the price moves constantly.

The second company is a relatively unknown and therefore may not attract market participant’s attention as there is no news or event surrounding this company. Under such circumstances, the stock price may not move or even if it does it may be very marginal.

To summarize, the price moves because of expectation of news and events. The news or events can be directly related to the company, industry or the economy as a whole. For instance the appointment of Narendra Modi as the Indian Prime Minister was perceived as positive news and therefore the whole stock market moved.

In some cases there would be no news but still the price could move due to the demand and supply situation.

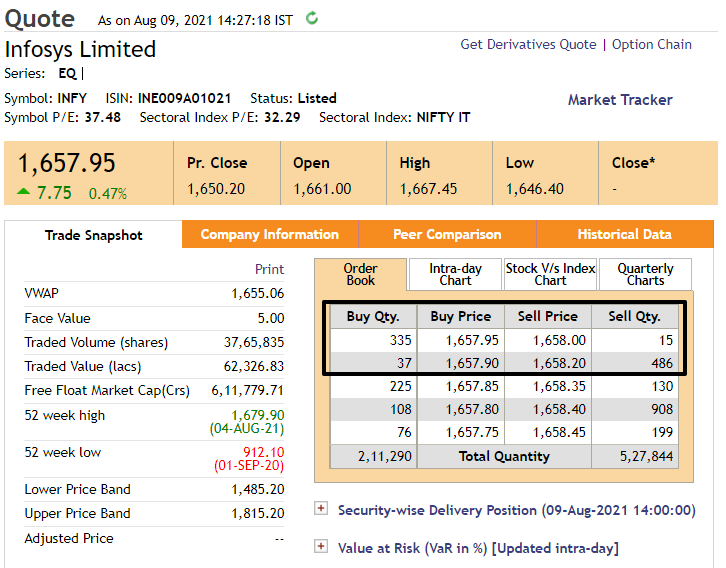

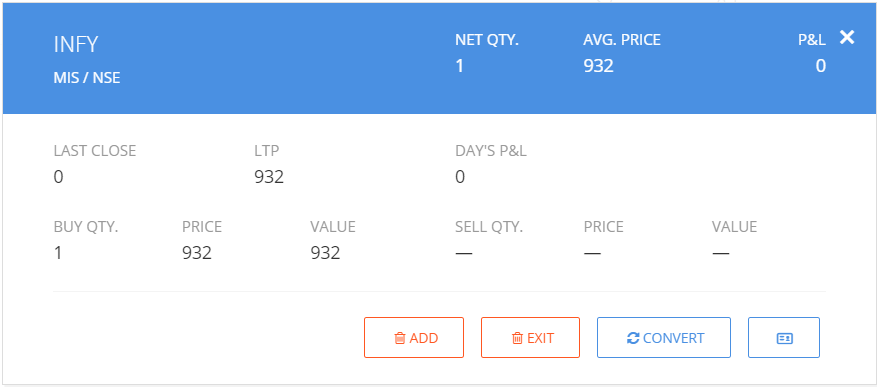

You have decided to buy 200 shares of Infosys at 3030, and hold on to it for 1 year. How does it actually work? What is the exact process to buy it? What happens after you buy it?

Luckily there are systems in place which are fairly well integrated.

With your decision to buy Infosys, you need to login to your trading account (provided by your stock broker) and place an order to buy Infosys. Once you place an order, an order ticket gets generated containing the following details:

Details of your trading account through which you intend to buy Infosys shares – therefore your identity is revealed.

The price at which you intend to buy Infosys

The number of shares you intend to buy

Before your broker transmits this order to the exchange he needs to ensure you have sufficient money to buy these shares. If yes, then this order ticket hits the stock exchange. Once the order hits the market the stock exchange (through their order matching algorithm) tries to find a seller who is willing to sell you 200 shares of Infosys at 3030.

Now the seller could be 1 person willing to sell the entire 200 shares at 3030 or it could be 10 people selling 20 shares each or it could be 2 people selling 1 and 199 shares respectively. The permutation and combination does not really matter. From your perspective, all you need is 200 shares of Infosys at 3030 and you have placed an order for the same. The stock exchange ensures the shares are available to you as long as there are sellers in the market.

Once the trade is executed, the shares will be electronically credited to your DEMAT account. Likewise the shares will be electronically debited from the sellers DEMAT account.

After you buy the shares, the shares will now reside in your DEMAT account. You are now a part owner of the company, to the extent of your share holding. To give you a perspective, if you own 200 shares of Infosys then you own 0.000035% of Infosys.

By virtue of owning the shares you are entitled to few corporate benefits like dividends, stock split, bonus, rights issue, voting rights etc. We will explore all these shareholder privileges at a later stage.

Holding period is defined as the period during which you intend to hold the stock. You may be surprised to know that the holding period could be as short as few minutes to as long as ‘forever’. When the legendary investor Warren Buffet was asked what his favorite holding period was, he in fact replied ‘forever’.

In the earlier example quoted in this chapter, we illustrated how Infosys stocks moved from 3000 to 3016 in a matter of 5 minutes. Well, this is not a bad return after all for a 5 Minute holding period! If you are satisfied with it you can very well close the trade and move on to find another opportunity. Just to remind you, this is very much possible in real markets. When things are hot, such moves are quite common.

Now, everything in markets boils down to one thing. Generating a reasonable rate of return!

If your trade generates a good return all your past stock market sins are forgiven. This is what really matters.

Returns are usually expressed in terms of annual yield. There are different kinds of returns that you need to be aware of. The following will give you a sense of what they are and how to calculate the same…

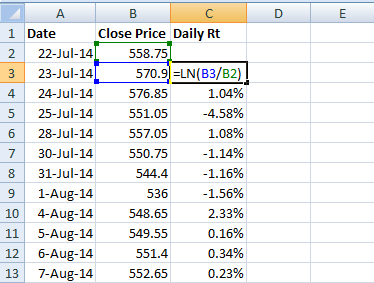

Absolute Return – This is return that your trade or investment has generated in absolute terms. It helps you answer this question – I bought Infosys at 3030 and sold it 3550. How much percentage return did I generate?

The formula to calculate the same is [Ending Period Value / Starting Period Value – 1]*100

i.e [3550/3030 -1] *100

= 0.1716 * 100

= 17.16%

A 17.6% is not a bad return at all!

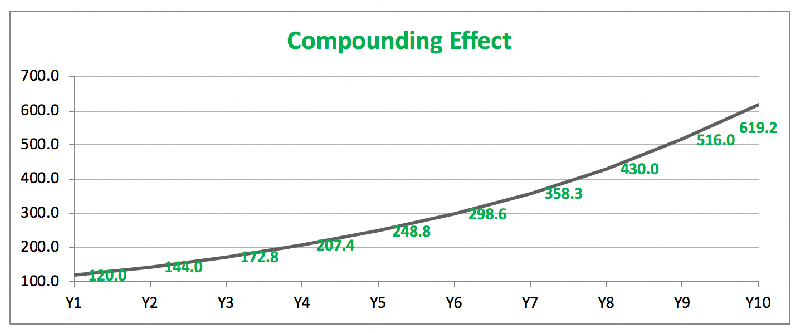

Compounded Annual Growth Rate (CAGR) – An absolute return can be misleading if you want to compare two investments. CAGR helps you answer this question – I bought Infosys at 3030 and held the stock for 2 years and sold it 3550. At what rate did my investment grow over the last two years?

CAGR factors in the time component which we had ignored when we computed the absolute return.

The formula to calculate CAGR is ..

Applying this to answer the question..

{[3550/3030]^(1/2) – 1} = 8.2%

This means the investment grew at a rate of 8.2% for 2 years. Considering the fact that Indian fixed deposit market offers a return of close to 8.5% return with capital protection an 8.2% return suddenly looks a bit unattractive.

So, always use CAGR when you want to check returns over multiple years. Use absolute return when your time frame is for a year or lesser.

What if you have bought Infosys at 3030 and sold it at 3550 within 6 months? In that case you have generated 17.16% in 6 months which translates to 34.32% (17.16% * 2) for the year.

So the point is, if you have to compare returns, its best done when the return is expressed on an annualized basis.

Each market participant has his or her own unique style to participate in the market. Their style evolves as and when they progress and witness market cycles. Their style is also defined by the kind of risk they are willing to take in the market. Irrespective of what they do, they can be categorized as either a trader or an investor.

A trader is a person who spots an opportunity and initiates the trade with an expectation of profitably exiting the trade at the earliest given opportunity. A trader usually has a short term view on markets. A trader is alert and on his toes during market hours constantly evaluating opportunities based on risk and reward. He is unbiased toward going long or going short. We will discuss what going long or short means at a later stage.

There are different types of traders :

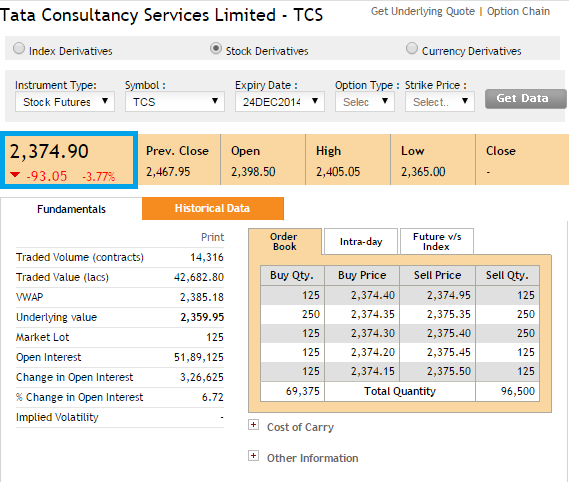

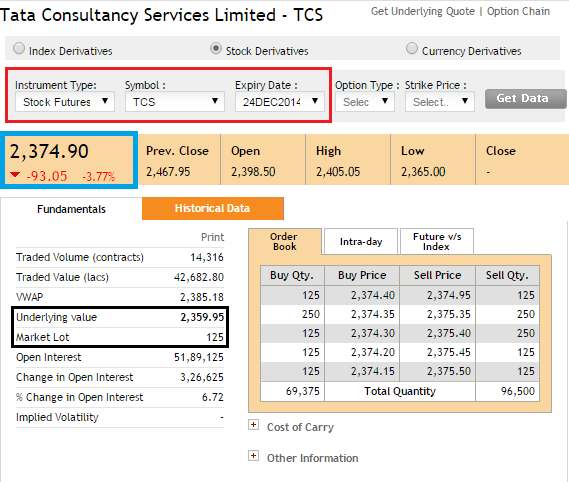

Day Trader – A day trader initiates and closes the position during the day. He does not carry forward his positions. He is risk averse and does not like taking overnight risk. For example – He would buy 100 shares of TCS at 2212 at 9:15AM and sell it at 2220 at 3:20 PM making a profit of Rs.800/- in this trade. A day trader usually trades 5 to 6 stocks per day.

Scalper – A type of a day trader. He usually trades very large quantities of shares and holds the stock for very less time with an intention to make a small but quick profit. For example – He would buy 10,000 shares of TCS as 2212 at 9:15 and sell it 2212.1 at 9.16. He ends up making 1000/- profit in this trade. In a typical day, he would have placed many such trades. As you may have noticed a scalp trader is highly risk averse.

Swing Trader – A swing trader holds on to his trade for slightly longer time duration, the duration can run into anywhere between few days to weeks. He is typically more open to taking risks. For example – He would buy 100 shares of TCS at 2212 on 12th June 2014 and sell it 2214 on 19th June 2014.

Some of the really successful traders the world has seen are – George Soros, Ed Seykota, Paul Tudor, Micheal Steinhardt, Van K Tharp, Stanley Druckenmiller etc

An investor is a person who buys a stock expecting a significant appreciation in the stock. He is willing to wait for his investment to evolve. The typical holding period of investors usually runs into a few years. There are two popular types of investors..

Growth Investors – The objective here is to identify companies which are expected to grow significantly because of emerging industry and macro trends. A classic example in the Indian context would be buying Hindustan Unilever, Infosys, Gillette India back in 1990s. These companies witnessed huge growth because of the change in the industry landscape thereby creating massive wealth for its shareholders.

Value Investors – The objective here is to identify good companies irrespective of whether they are in growth phase or mature phase but beaten down significantly due to the short term market sentiment thereby making a great value buy. An example of this in recent times is L&T. Due to short term negative sentiment; L&T was beaten down significantly around August/September of 2013. The stock price collapsed to 690 all the way from 1200. At 690 (given its fundamentals around Aug 2013), a company like L&T is perceived as cheap, and therefore a great value pick. Eventually it did pay off, as the stock price scaled back to 1440 around May 2014.

Some of the really famous investors the world has seen – Charlie Munger, Peter Lynch, Benjamin Graham, Thomas Rowe, Warren Buffett, John C Bogle, John Templeton, etc.

So what kind of market participant would you like to be?

If I were to ask you to give me a real-time summary of the traffic situation, how would you possibly do it?

Your city may have 1000’s of roads and junctions; it is unlikely you would check every road in the city to find the answer. The wiser thing for you to do would be to quickly check a few important roads and junctions across the city’s four directions and observe how the traffic is moving. If you observe chaotic conditions across these roads, you would simply summarize the traffic situation as chaotic, else traffic can be considered normal.

The few important roads and junctions that you tracked to summarize the traffic situation served as a barometer for the entire city’s traffic situation!

Drawing parallels, if I were to ask you how the stock market is moving today, how would you answer my question? There are approximately 5,000 listed companies in the Bombay Stock Exchange and about 2,000 listed companies on the National Stock Exchange. It would be clumsy to check every company, figure out if they are up or down for the day and then give a detailed answer.

Instead, you would just check a few important companies across key industrial sectors. If a majority of these companies are moving up, you would say markets are up, if the majority is down, you would say markets are down, and if there is a mixed trend, you would say markets are sideways!

So essentially identify a few companies to represent the broader markets. Every time someone asks you how the markets are doing, you would just check the general trend of these selected stocks and then answer. These companies that you have identified collectively make up the stock market index!

Luckily you need not actually track these selected companies individually to get a sense of how the markets are doing. The important companies are pre-packaged and continuously monitored to give you this information. This pre-packaged market information tool is called the ‘Market Index’.

There are two main market indices in India. The S&P BSE Sensex representing the Bombay stock exchange and CNX Nifty representing the National Stock exchange.

S&P stands for Standard and Poor’s, a global credit rating agency. S&P has the technical expertise in constructing the index which they have licensed to the BSE. Hence the index also carries the S&P tag.

CNX Nifty consists of the largest and most frequently traded stocks within the National Stock Exchange. It is maintained by India Index Services & Products Limited (IISL), a joint venture of the National Stock Exchange and CRISIL. In fact, the term ‘CNX’ stands for CRISIL and NSE.

An ideal index gives us minute by minute reading about how the market participants perceive the future. The movements in the Index reflect the changing expectations of the market participants. When the index goes up, it is because the market participants think the future will be better. The index drops if the market participants perceive the future pessimistically.

Some of the practical uses of Index are discussed below.

Information – The index reflects the general market trend for a period of time. The index is a broad representation of the country’s state of the economy. A stock market index that up indicates people are optimistic about the future. Likewise, when the stock market index is down, people are pessimistic about the future.

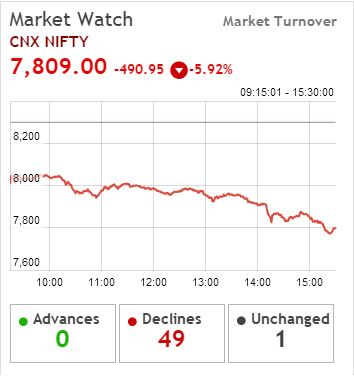

For example, the Nifty value on the 1st of January 2014 was 6301, and the value as of 24th June 2014 was 7580. This represents a change of 1279 points in the index of a 20.3% increase. This simply means that during the time period under consideration, the markets have gone up quite significantly, indicating a strong optimistic economic future.

The time frame for calculating the index can be for any length of time. For example, the Index at 9:30 AM on 25th June 2014 was at 7,583, but an hour later it moves to 7,565. A drop of 18 points during this period indicates that the market participants are not too enthusiastic.

Benchmarking – For all the trading or investing activity that one does, a yardstick to measure the performance is required. Assume over the last 1 year you invested Rs.100,000/- and generated Rs.20,000 return to make your total corpus Rs.120,000/-. How do you think you performed? Well on the face of it, a 20% return looks great. However, what if Nifty moved to 7,800 points from 6,000 points generating a return on 30% during the same year?

Well, suddenly it may seem to you that you have underperformed the market! If not for the Index, you can’t really figure out how you performed in the stock market. You need the index to benchmark the performance of a trader or investor. Usually, the objective of market participants is to outperform the Index.